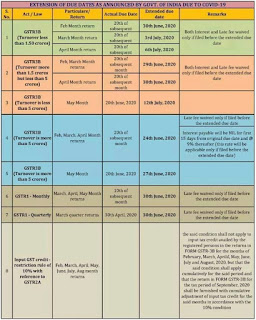

AMENDMENTS IN CGST RULES

Other than extension of dates for

GST returns, some important amendments to CGST Rules 2017 have been covered as

follows:

1. Registration: In an

attempt to centralize data of an entity on records with government Authentication

of Aadhar Number is mandatory while obtaining GST Registration

filing from 1st April 2020. In cases, if the applicant does not have PAN Number

in such cases, the application can be accepted only on physical verification at

the principal place of business in the presence of the applicant within 60 days

from the date of filing of the application. However, Aadhar authentication for

the obtaining GST registration from 1st April 2020 does not apply to a person

who is not a citizen of India and to any other class of persons not mentioned

below:

1. Individual

2. Authorized

Signatory of all types

3. Managing and

Authorized Partner

4. Karta of a

Hindu Undivided Family

2. Physical Verification in

Certain cases: In order to correct cases of fake invoicing on

addresses which are not in existence, if the officer feels that physical

verification is required for the principal place of business for any other

reason or the applicant does not have the PAN Number, the verification report

along with the photographs and other documents has to be uploaded on the common

portal within 15 days of such physical verification using the Form GST REG –

30.

3. Input Tax Credit on Capital

Goods: The life of capital goods for the GST purposes is considered to be

five years from the date of invoice, and the amount of tax shown on the tax

invoice will be reflected in the input tax credit ledger. The input tax credit

claimed has to be reversed at the rate of 5% per quarter is the capital

goods are used for other than taxable supplies. The tax to be reversed has to

be computed separately for each tax and reported in GSTR – 3B.

4. GST Audit Threshold Limit

for FY 2018-19: The GST Audit threshold for the financial year 2018-19 has

been increased to Rs 5 crores in order to reduce the compliance burden

on small retailers, traders, shop keepers who comprise the Medium, Small and

Micro Enterprise (MSME) sector, the Union Budget proposed to raise by five

times the turnover threshold for audit from the existing Rs. 1 crore to Rs. 5

crore.

5. Refund of excess payment of

Taxes: If the registered taxpayer has claimed refund of the taxes paid in

excess or paid wrongly in different heads, for which debit has been made from

the electronic credit ledger, earlier, after inspection by GST authorities, refund

amount was credited to the applicant bank account which lead to many

fraudulent cases seeking cash against credit wrongly taken, which later even if

government comes to know about can’t be corrected and even liquidity was lost . Currently government has kept on hold such refunds where they had doubt and asked assessees to show documents to verify and justify their claim. To check this, now refund amount shall be re-credited to the electronic credit

ledger by the proper officer through FORM GST PMT-03.

6. Zero Rated Supplies:

Turnover for Zero Rated Supply has been defined, and it means the value of

zero-rated supplies made during a relevant tax period under letter of credit or

bond or the value which is 1.5 time of the value of like goods domestically

supplied by the same or, similarly placed, supplies as declared by the supplier

whichever is lesser. The change is made to ensure that undue excessive refund

on itc calculated by the formula using turnover for Zero rated supply is not

made by the assessee.

7. Recovery of Refund: GST

Law regarding refund for export of goods or services or both was not in line

with FEMA Foreign Exchange Management Act ,1999 where time limit for realizing

export proceeds were specified. Taking advantage of this loophole, many

exporters made money by seeking refund against fake shipping bills and export

documents. In order to correct this practice, the taxpayers who have claimed a

refund for export of goods or services or both have not realized the value of

the goods or services exported based on the time limit prescribed under Foreign

Exchange Management Act 1999, the amount of refund claimed has to be paid with

interest for the pro-rated amount which is not realized. The amount has to be

remitted within 30 days of the expiry of the time period prescribed else the

recovery proceedings will be initiated under Section 73 or Section 74 of the

CGST Act 2107. Where the sale proceeds have been written off by the Reserve

Bank of India, in such cases, no recovery will be made. The amount of refund

recovered from the taxpayer for non-realization will be refunded back if the

exporter pays back the amount. The amount will be refunded if the exporter

claims the same within three months from the date of remittance along with

valid proofs.

Comments

Post a Comment